Most Kiwis believe they won’t have sufficient retirement funds and for many Kiwis, they’re right.

Having financial security in retirement is critical, as without it retirees may have a poor quality of life and a lack of choices, from where to live to accessing healthcare.

By 2050 the number of over 65’s will have doubled (Te Ara Ahunga Ora). Research from the UK has shown that, globally, ‘in all developed economies, there has been a gradual shift in responsibility for social protection of individual citizens from the state to the individuals themselves (Financial Well-Being A Conceptual Model and Preliminary Analysis, 2017)’ .

This shift has consequences, as ‘citizens must operate in an increasingly complex financial marketplace to meet their own social protection needs and those of their household’ and ‘this has raised concern about the extent to which they are equipped to do so’.

This shift will ‘affect Kiwis standard of living in retirement (Mercer CFA Institute Global Pension Index 2022)' .

In New Zealand, KiwiSaver is the retirement savings plan for most New Zealanders. It came into existence in 2007 and by 2011 there were around 1.7 million members and assets totalling $9.1 billion (FMA, 2011). Fast forward to reporting in 2023 and those figures grew to 3.25 million KiwiSavers and $93.7 billion saved (FMA, 2023).

It is a scheme that has seen considerable growth. However, with an average balance of $28,778 in 2023, is it really making sure all generations of Kiwis are prepared for retirement?

Over 70% of respondents to a 2021 FSC survey thought they would need to work past retirement age to fund their retirement. The same survey reflected that 65% of respondents thought they were not on track to have enough money for a happy retirement or be able to afford where they live when they retire.

Coupled with the need to balance paying for today and saving for tomorrow, it is hard to save for the future and to predict how much retirement might cost.

We have differing levels of what we expect - some might look to spend their retirement travelling, others might choose (or need) to continue work or volunteer at home.

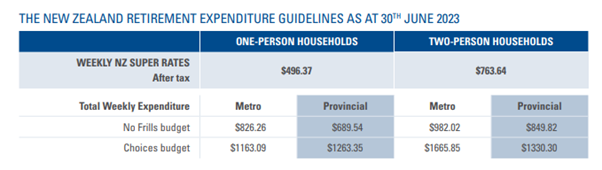

A useful guide is Massey University's yearly New Zealand Retirement Expenditure Guidelines, where a guide provides how much weekly retirement expenditure is needed in New Zealand.

The guidelines offer a ‘basic’ or ‘no frills’ and a more comfortable ‘choices’ calculation for metro and provincial single and couple retirees based on current retirement expenditure needs. It shows that most New Zealanders already need to have more income than the current weekly NZ Super provides.

Figure 1: The New Zealand Retirement Expenditure Guidelines as at 30th June 2023

Since the 2022 report, there has been around a 5 - 6% growth in expenditure needs and as the 2023 report theme suggests, ‘retirement planning [is] a moving target’ as economic cycles affect saving levels for retirement.

The headline '3.25 million KiwiSaver members and $93.7 billion asset numbers' looks good on the surface. But dig beneath the figures and we see that active participation and contribution rates aren’t going to meet our individual needs when we reach 65, especially for younger generations.

Planning and saving for retirement is getting more difficult on one hand, but is a necessity on the other.

Considering this, industry and government need to look together at how we can help improve retirement policy settings and financial literacy for retirement saving, so that we can work to ensure that all Kiwis have a dignified retirement. See our document Blueprint for Growth for our priorities to achieve this.